Engineering Net Zero Part 9C: Strategy Options for our Future Energy System

David Simmonds continues his mini-series by looking at some of the unintentional consequences of strategy decisions, and recommends hybrids as a long-duration DSR measure

HAVING written about new ways to present the technologies for energy system balancing (Part 9A) and modelling (Part 9B), I would like to conclude this extension to the ENZ series by looking at some of the challenges facing the National Energy System Operator’s Clean Power 2030 alternatives and their Future Energy Scenarios for 2050. The National Energy System Operator (NESO) are well on top of their programme for short-duration measures including short-duration demand side response (DSR), but I believe we require more detail on their plans for long-duration balancing to meet the 15-20% challenge. In the last feature I touched on the need to review the UK’s energy marketing model in order to realise competitive electricity pricing to drive electrification, but we must go further and relook at the merits of the proposed power import/export strategy and better frame the options for domestic heating, so I offer an alternative long-term strategic option.

Seen in isolation, decisions on heating and interconnectors can be obvious or trivial, but once one looks at the operation of a system it is not necessarily so. For example, the installation of an efficient 10 kW heat pump, operating at 50% load during the year, requires installation of 12 kW of offshore wind capacity and almost 10 kW of back-up capacity. Why?

The operational efficiency of offshore wind is between 40–45% and therefore over the year some 12 kW of offshore wind capacity is needed to satisfy the 5 kW average consumption. However, supply must be balanced to use, requiring back-up power capacity, and, as the heat pump will operate during periods of little or no wind, 10 kW of installed back-up capacity is also required. In other words, this simple domestic heat pump requires over twice its rated capacity in installed generation capacity or, put another way, backing up renewables adds inefficiency, complexity, and cost – leading to unintended consequences?

As to the extended use of interconnectors, beyond the value loss argument presented previously, I believe we could be offshoring emissions, so let me start there.

Extending use of interconnectors to balance our energy grid

In Part 9A with the Power System Onion, I discussed and questioned the use of interconnectors to export surplus summer power and import electricity during the winter to offset shortages.

The first interconnector to France came onstream in 1986, but since 2011 we have seen more commissioned to strengthen resilience. Over the last year, imports through these interconnectors rose to 15% of the UK’s power needs, reducing our dependence on fossil gas. Half of those imports originated from France with its massive nuclear programme, enabling us to enhance our green credentials.

Since Brexit, the trading arrangements for imports have deteriorated. Further, one can expect that imports are contributing to the UK having among the highest electricity prices in Europe. A recent House of Commons research briefing notes: “In the first half of 2024 UK domestic electricity prices were higher than in all but three EU countries.” Much of the blame for high electricity prices is laid at the door of our dependency on international gas to balance our power supplies, but the same report states that “gas prices in the UK were 22% below the EU average”.

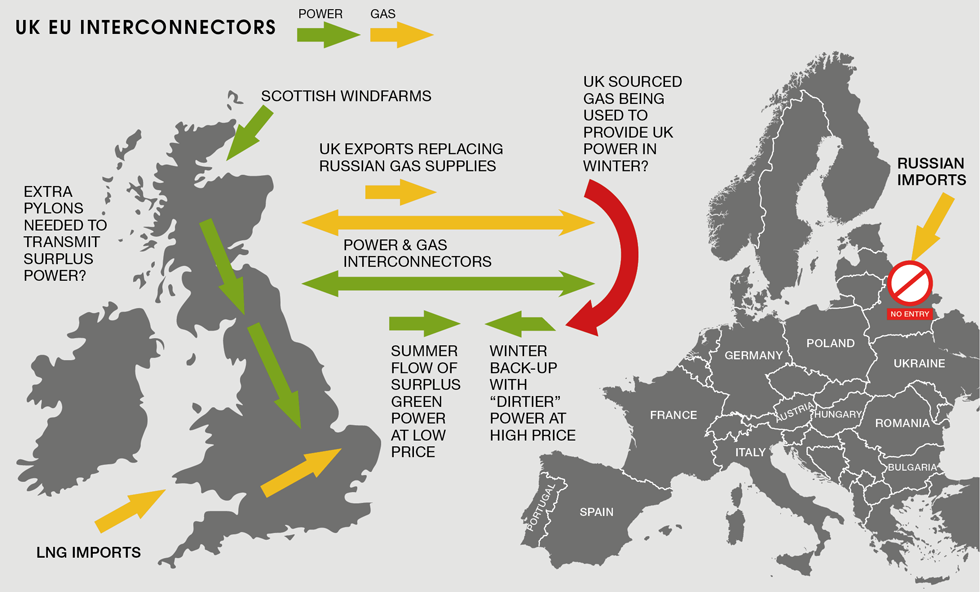

As we look forward to 2030 and 2050, with renewables meeting most demand, the NESO scenarios rely on power exports to manage surpluses, and imports to alleviate shortfalls (ie when the wind does not blow), managing much of the 15–20% challenge. I would question the merits of this strategy through deliberation on the chart below, which considers the interaction of gas and power networks.

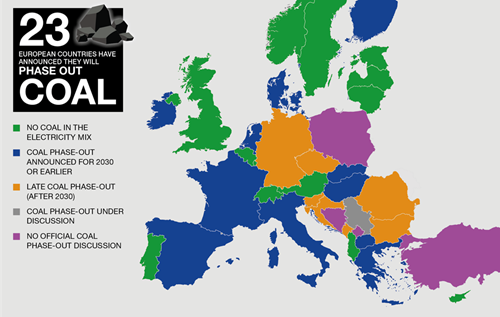

If I start with gas flows, following the Ukraine war, Europe terminated much of its Russian supplies, replacing them with liquefied natural gas (LNG) imports. Without terminal capacity, Europe imported significant volumes through the UK’s high-capacity import terminals, receiving it through the gas interconnectors. This continues today and is one reason why gas is cheaper here than in Europe. In Europe, some of that gas is used to generate power, and this will still be the case in 2030, for Europe as a whole will not have achieved equivalent Clean Power 2030 targets. Worse, some countries interconnected across Europe will still be producing power from coal – see above (courtesy of BeyondFossilFuels.org). We can anticipate that when we need to import, demand across Europe will also be high, so, on a marginal basis, our imports will most probably have been produced by 100% fossil fuel. Consequently, one can question whether it would be better to directly fire our own gas-powered stations at lower cost, higher efficiency and potentially lower emissions; hence to my earlier question – are we offshoring emissions?

Moving to electricity, I also have concerns over the strategy to export surpluses. The recent Panorama programme with Justin Rowlatt, The Race to Go Green, highlighted the plight of Scottish residents fighting pylon construction across the Highlands. These and much of the grid down through the country to East Anglia and the south coast will be sized to transmit peak outputs to avoid curtailment fees. However, given the operational efficiency of offshore wind is in the order of 40–45%, much of the grid will be operate at similar or lower utilisation rates. Further, as mentioned earlier, one can question the price the UK will receive for these exports. Indeed, in a recent quarterly Drax Electric Insights report, Iain Staffell a lecturer in sustainable energy at the Centre for Environmental Policy, noted: “There’s been a huge rise in the volume of solar power capacity installed on the continent. Germany has installed 14 times as much solar capacity in the last three years as the UK to cut its reliance on Russian gas. That means in spring and summer months there is often an abundance of cheap electricity on the continent which the UK can import.” Does this support an interconnector export strategy?

When challenged to meet the government’s Clean Power target for 2030, I can see NESO had little choice. However, I would suggest that the UK government needs to reconsider its strategy if it prolongs today’s high price differential and increases overall emissions.

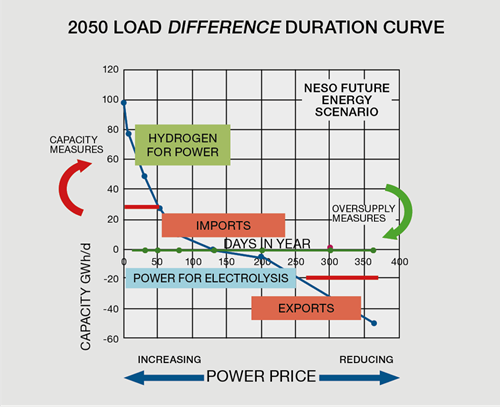

The continuation of an interconnector-based import/export strategy through to 2050 must definitely be questioned. The LDDC format discussed in Part 9B can be used to present the 2050 scenario as shown here where the interconnectors are supported through limited application of the hydrogen cycle (as described in Parts 9A and 9B).

The alternative is more extensive use of hydrogen for balancing, especially as this means we will be independent of foreign energy. Given NESO sees that hydrogen will be necessary to manage the final 5% of demand, it should consider extending hydrogen for the full 15–20% challenge. This is much as considered by the Royal Society and Imperial College in their Hydrogen Futures report, while the Industrial Decarbonisation Research and Innovation Centre (IDRIC) is already undertaking studies for hydrogen storage to support industrial demand. Critics will argue, rightly, that the hydrogen cycle is inefficient, but as we have seen the interconnector strategy has its own inefficiencies with low utilisation of high voltage grid infrastructure. These observations segue nicely to the need to consider hydrogen’s role in hybrid heating which can improve low voltage grid utilisation.

Benefits of hybrid heating on power system design

Currently, UK government policy is being used to drive the consumer transition, terminating sales of internal combustion engine vehicles and gas boilers over the next decade. However, today, replacement technologies are more expensive, and the government must address the spark gap, the price ratio of electricity to gas, in order to incentivise heat pumps, and consider more incentives to support the transition to EVs.

In ENZ 2 and 3 I raised hydrogen hybrid options for heating and transport as these offer consumers more choice, reduce the one-basket risk of full electrification, and lower costs. Here I will focus on heating as this is subject to a UK policy decision next year, and has a greater impact on power grid design and operation. A hydrogen hybrid heating system, a heat pump with small hydrogen gas boiler, only utilises the hydrogen boiler during cold weather or when power supplies are tight. With variable pricing, consumers can manage their costs by switching to hydrogen boiler mode at times of high power demand to offset peak prices. Indeed, AI and other smart technologies can be deployed to manage energy use in hybrid heating for the benefit of consumer and system operator alike.

In their studies on electricity storage, the Royal Society noted that the hydrogen cycle, with its electrolysis, storage and hydrogen peaker loop, is only the order of 40% efficient. The significant part of the inefficiency comes from the last stage, hydrogen to power, typically using what are termed hydrogen peakers; direct use of stored hydrogen to offset peak power demand would be beneficial.

Going back to my 10 kW heat pump example, a consumer with a 10 kW hybrid heat pump still needs the 12 kW renewable supply capacity but the 10 kW back-up power capacity is no longer necessary as it is replaced by using the boiler. In the context of the Power System Onion, we can represent hybrid technologies as long-duration DSR measures, countering need for hydrogen peakers, as shown here in an update to the Power System Onion.

Readers will recognise that hybrid heating requires conversion of the gas grid to hydrogen service, and that this will be both expensive and a major project in its own right. However, the earlier discussion on the Power System Onion only considered the generation of supplies to match demand, we have yet to consider the impact peak power demands from heat pumps and EVs will have on local LV distribution grids.

Short-duration DSR measures, including phased EV charging, and battery systems will level out local grid demand, but, as the onion shows, we still require reinforcing measures to manage peak demand. LV distribution grids are not sized for tomorrow’s heat pumps, which, during cold weather, will run continuously and simultaneously. Full electrification will require major upgrades to local transmission grids, and Energy Futures Lab, in their Delivering Our Future Power System progress report, red-flagged local distribution as strategies for this have yet to be developed. This was also the focus for the recent National Infrastructure Commission (NIC) report on investment in electricity distribution networks where Sir John Armitt quotes: “We must learn the lessons from playing catch-up on transmission grid expansion and get ahead of the curve on investing in our local networks.”

I fully agree with hydrogen critics that widespread hydrogen heating is not viable due to the cost of hydrogen, but full electric heating, even with heat pumps, will be prohibitive for many and require major upgrades to both HV and LV grids.

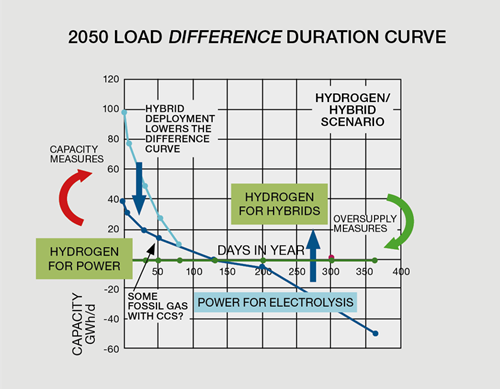

With hybrid heating, hydrogen is used directly to offset peak power demand, and becomes a long-duration DSR measure, significantly reducing the need for power grid upgrades, but, more importantly for consumers, it will reduce heat pump installation and running costs. The impact of hybrids can also be shown on a LDDC as presented here with hybrids reducing the level of the difference curve and the quantum of stored power.

Coincidentally a retired heating engineer recently passed me a little booklet he is preparing, sharing his lifetime experience of designing and installing green heating solutions for customers. Interestingly, many of his case studies considered selection of a hybrid heat pump (today using natural gas) in order that his customers did not have to undertake major structural changes to their property, even though this meant they did not qualify for a heat pump installation grant. Without a grant, hybrids were cheaper.

Hydrogen may have another use in heating as a Dutch colleague led me to Cooll, a company based in the Netherlands developing an efficient hydrogen-fuelled heat pump.

A strategy alternative

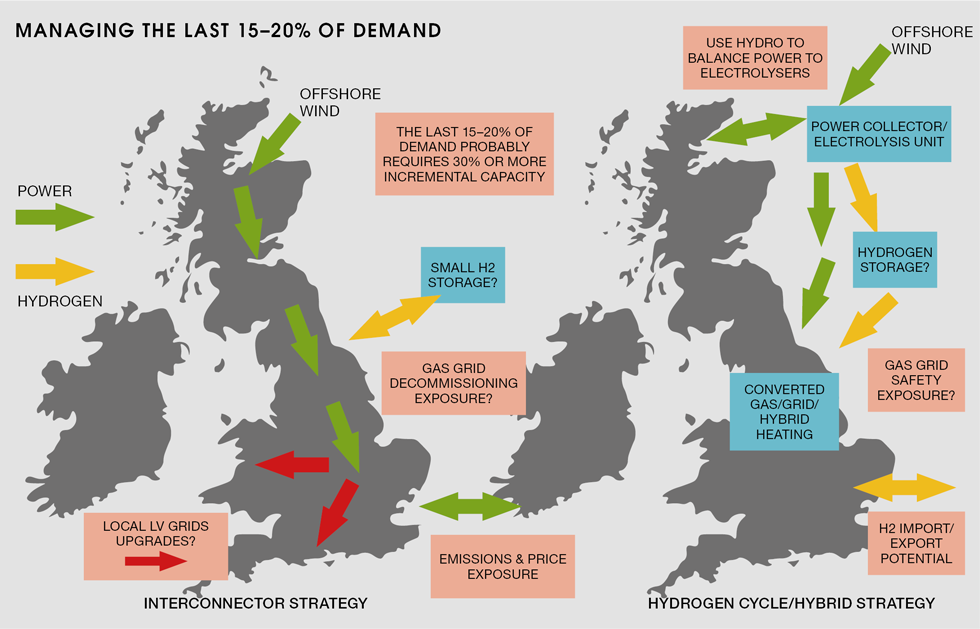

NESO’s planning for short-duration measures to increase the operability of the system is well covered in their options for 2030 and scenarios for 2050. However, as we have seen, their preferred scenarios for long-duration balancing consider imports/exports and electrified heating. Given my concerns, I conclude this extension to ENZ by comparing it in the chart below to a hydrogen cycle/hybrid technology alternative to meet the 15–20% challenge, 15% in a typical year, 20% in a design year. The core scope utilising renewables remains much as per NESO's plans, but, as we have seen through the last two features, it is this last tranche that really impacts system costs and design.

The chart captures some of the key considerations for two options which although based upon similar development of renewables result in very different infrastructure requirements. Many of those considerations have already been discussed in this series, but some pertinent summary points are considered below:

Interconnector/electrification strategy

- Full electrification requires extensive expansion of both HV (green arrows) and LV (red arrows) grid systems. Although we are considering the last 15–20% of demand, the shape of the supply duration curve is such that we can anticipate 50% or more incremental grid capacity to cater for peak supplies/demand, reducing investment efficiency in grid capacity measures

- It is dependent upon non-cyclical power imports, which have questionable sustainability, emissions loadings, and carry security of supply risks, with exports occurring at times of low pricing

- It still requires some hydrogen investment to meet the final 5% of demand, and requires a strategy for gas grid decommissioning

Hydrogen cycle/hybrid strategy

- This replaces power imports/exports by extending use of the hydrogen cycle for the full 15–20% challenge

- It requires conversion of the gas grid and more extensive offshore storage of hydrogen. To be viable, engineers must present a positive hydrogen safety appraisal before a decision can be made, currently planned for 2026

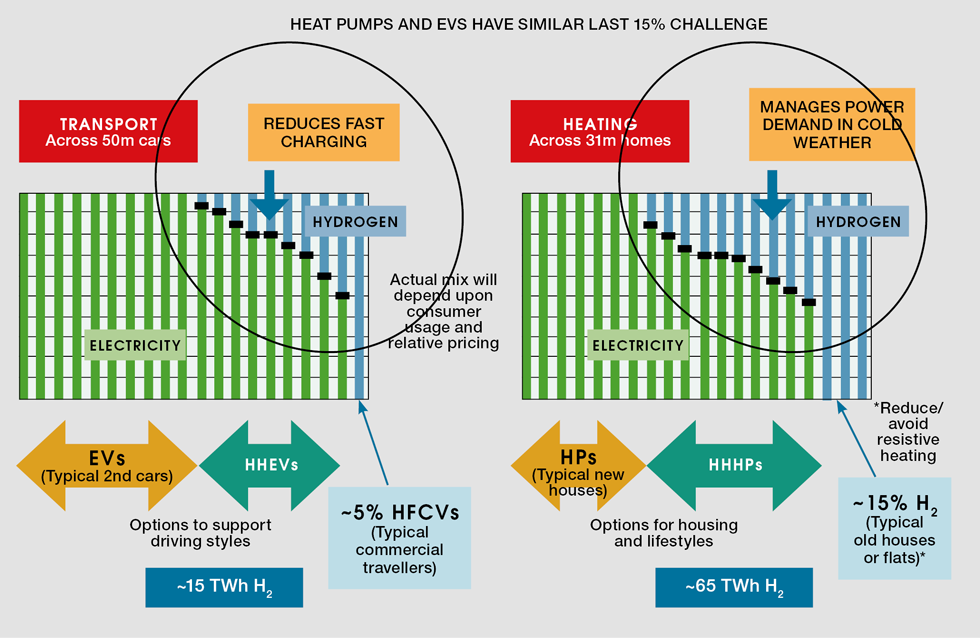

- The below chart, taken from ENZ8, attempts to show how hybrid heating and transport operate at a consumer level. It demonstrates how hydrogen usage zones can significantly reduce investment in LV distribution, , and it also indicates that likely hydrogen usage for the two technologies would only be in the order of 80 TWh, matching anticipated energy storage

- Germany and the Netherlands are already in advanced stages of developing a hydrogen grid, and we could reinforce our future energy system through conversion of gas interconnectors for hydrogen imports/exports

- A recent TCE article highlighted recent work on offshore power/hydrogen hub concepts. These can look to placing more infrastructure offshore, reducing the scope for grid pylons

- Many raise concerns over the slow uptake of green hydrogen, but this is inevitable until such time as renewables are supplying 80+% of demand, for currently we don’t have surplus power. However we will soon pass this point and so must urgently plan for a sustainable energy solution such as the hydrogen cycle

General points

- Planning and system development must consider design winters

- System planning and policy setting should also test other possible mitigations including more investment in efficiency measures, carbon capture, cheaper nuclear, fusion, and eventually hydrogen or ammonia imports, the latter replicating the role LNG successfully plays today

One of NESO’s alternatives for Clean Power 2030 includes adding carbon capture on fossil fuel generation. Extending this to manage the risk of over-optimistic delivery of renewables and associated balancing measures, will reduce costs and could benefit from synergies with the UK’s industrial clusters’ carbon capture plans.

We face big decisions, requiring rigorous stochastic analysis, economic, and risk assessment. Further, the assessment must consider the impact on consumers, be it pylons, home heating, transport, safety, lifestyle changes, offshore impact, and costs. Without a database, I am not in a position to complete further detailed analysis of the alternatives, but our system planners must deliver a system which consumers can both live with and afford.

Since authoring this series I have applied both the Power System Onion and LDDC to my household energy system where we have invested in a solar PV system. Its payback is currently over 15 years, but I anticipate this will become much longer once variable pricing comes standard. Further investment in a heat pump will only be warranted once we have an agreed way forward with hybrid technologies, especially as a standalone heat pump will require the local grid operator to upgrade our local network.

Renewables, heat pumps, and EVs are all great technologies until you hit the 15–20% challenge, and, I strongly believe, NESO, the National Infrastructure Committee, Climate Change Committee (CCC), and others have yet to fully address its impact. Given the complexity of system modelling this is not surprising, for it is difficult to appreciate all the implications of “keeping the lights on” or the unintended consequences, such as the inefficiency of grid infrastructure, offshoring of emissions, and reliance on imported power. However, I hope the insights and strategic options developed in this series, will allow policy advisors to better appreciate and share the challenges, opportunities and alternatives. In particular, I believe the recent statements from the CCC that they foresee no use for hydrogen in domestic heating or transport, are unhelpful. Closing down options will lead to higher costs and impair the winning over of hearts and minds of what is potentially becoming a culture war. As far as I can see their conclusion comes from a hydrogen vs electrification comparison and not a hydrogen with electrification assessment as recommended in ENZ8 and further deliberated upon here.

When I presented a shortened version of these considerations in The Times recently, one correspondent summed it up as follows: “Use the wind to produce hydrogen and store it. Job done. It’s just what nature did for us creating natural gas, but without the climate side-effects.”

Recent Editions

Catch up on the latest news, views and jobs from The Chemical Engineer. Below are the four latest issues. View a wider selection of the archive from within the Magazine section of this site.