Engineering Net Zero Part 8: Electricity plus Hydrogen, not Electricity or Hydrogen

David Simmonds concludes his online series with a call for greater systems analysis to develop a credible hybrid plan for net zero energy

OVER seven features, which can be accessed online,1 I have been on a journey from the collaboration required to deliver net zero through to the options needed to give consumers more choice. Since I started the Engineering Net Zero (ENZ) series we have witnessed the warmest year on record, a cost-of-living crisis, and increasing pushback on net zero due to its perceived cost. I have explored synergies between sectors, identified potential roadblocks such as resources and skills, before addressing how we can deliver an energy system which is both affordable and reliable.

As mentioned in my last feature, we must satisfy the “quadlemma” – decarbonisation, while minimising cost, ensuring security of supply, and retaining international competitiveness – addressing the energy system from supply to demand. Or, as my old company, BG, had as its strapline, “From Resources To Markets”.

Doing nothing appeals to many, while policymakers are attracted by the “silver bullet” of a fully electrified energy system. In my view, neither is viable. I propose a multi-vector solution, using hybrid technologies to secure wider appeal. In the final feature in the series, I describe how those hybrid technologies can deliver and summarise earlier conclusions by providing my ENZ recommendations.

Today’s energy system

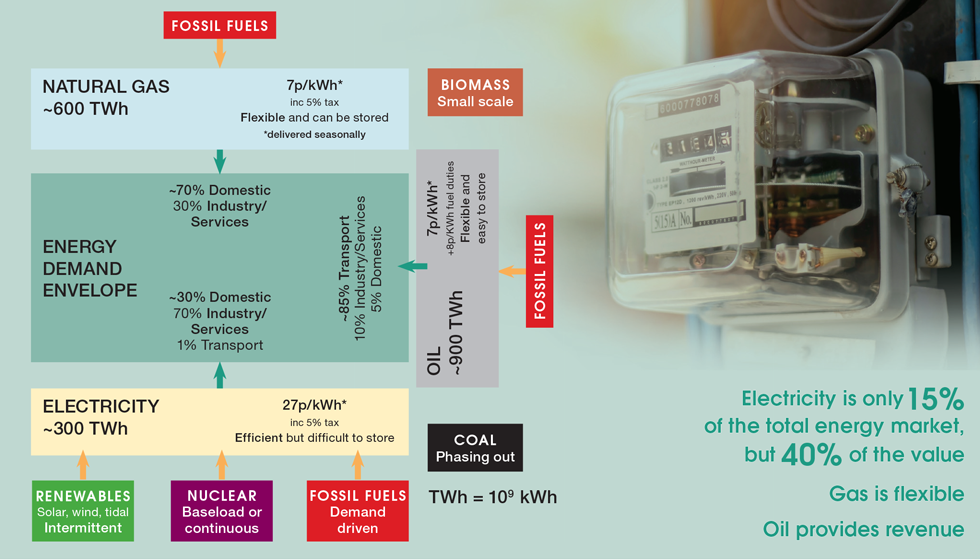

We should start by looking at the current UK energy system, depicted in Figure 1, which, in spite of all the claims, still relies on fossil fuels for approximately 80% of total demand.

There are three primary vectors; oil, meeting half of our total energy demand, primarily for transport; natural gas, meeting a third of demand, primarily for heating on a seasonal basis; and electricity. The latter is significantly more expensive and only provides one-sixth of today’s energy and is produced to demand as it cannot be stored easily. Traditionally generated from coal, then oil, and latterly from natural gas and nuclear, electricity is increasingly produced from renewables at lower cost but delivered on an intermittent basis. Demand has dropped over the last two decades as we have improved energy efficiency and outsourced much of our industry. This trend will reverse as we deploy efficient and cleaner technologies such as heat pumps and electric vehicles (EVs), adding seasonal demand and requiring major expansions of our power grid.

Low cost oil and gas dominate the transport and heating markets and governments leverage the low oil prices to raise duties on transport. Commoditisation of gas has allowed the UK to import gas to meet seasonal heating demand. However, during the run-up to the Russia-Ukraine war we witnessed significant supply disruption leading to price spikes. Prices have now returned to more normal levels, restoring the “spark gap” differential between the cost price of electricity and gas, and reducing the incentive to adopt efficient technologies. As EVs increase market share, governments will have to look at alternative ways of raising revenue, with heat pumps yet to prove economical alternatives to natural gas boilers. Here in the UK, coal is all but phased out, though India and China are continuing to increase their demand for this more polluting fuel. Biomass remains a niche energy resource, and there are concerns about its true sustainability.

This short introduction has highlighted a number of challenges for energy system planning:

- relative low cost of fossil fuels, presenting a hurdle for clean technologies

- intermittency of renewables and variable heating demand requires system balancing

- increasing demand which will delay decommissioning of legacy power generation

- growing seasonality of power demand from heat pumps, requiring more storage

- need to widely distribute power to meet EV charging and heat pump demand

- generating alternative state revenue as oil is phased out

- retaining the UK’s competitive position, globally

- providing incentives for cleaner technologies to meet climate change targets

Designing our future energy system

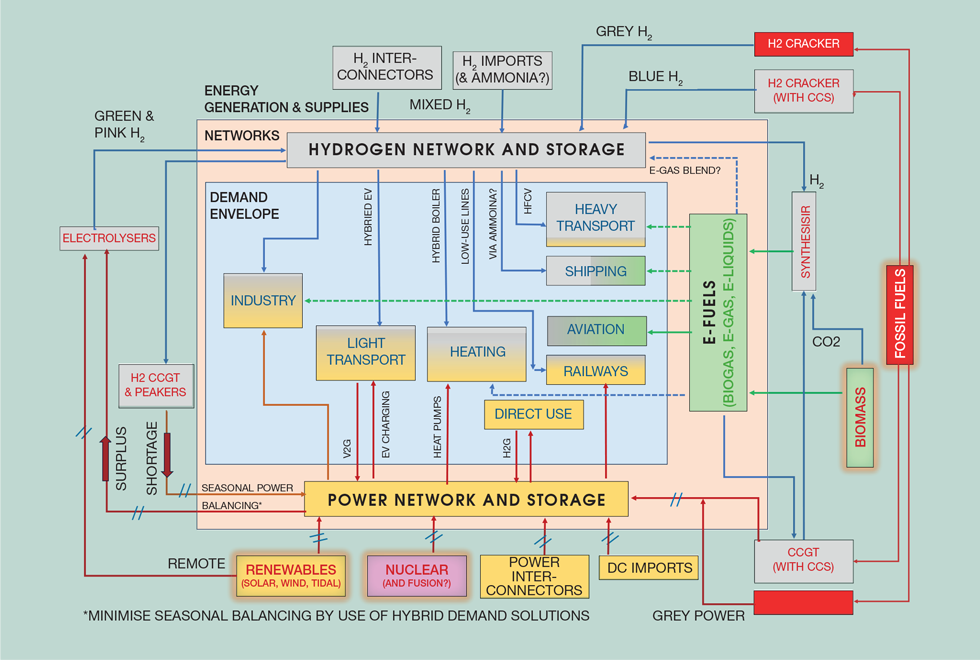

In my last feature – Energy Security and Affordability – I introduced the schematic (see Figure 2) depicting our future energy system.

This has a similar construct to today’s model with three main vectors: electricity, hydrogen, and e-fuels. Electricity will become the primary vector, with hydrogen and e-fuels, respectively, replacing natural gas and oil, both destined for harder to convert sectors. It is a complex diagram but serves four purposes: identifying primary resources, including the transition from fossil fuels (around the edge); markets (within the blue Demand Envelope); networks and storage (beige rectangle); and energy balancing (on the left).

In my last feature I highlighted the need for system modelling and noted some organisations and universities with this capability. It is imperative that this is done well, and the UK and US are fortunate to have some of the best modellers. However, they are often constrained by the requesting organisation, limiting alternatives studied and requiring compliance to policy without necessarily testing feasibility, aspects which came home to roost with the similarly complex HS2 rail project. As an example, National Grid, in their Future Energy Scenarios2 modelling, forecasts 20% of all electricity produced in 2050 be exported via interconnectors to balance the system – sold at what price?

Energy resources

Renewables will be at the heart of our future energy system, as they can reduce energy costs. However, while costs of components may drop, we are cherry-picking deployment, locating offshore wind turbines in shallow water for example, and costs will escalate as we deploy floating turbines. Further, they operate intermittently, and in my last feature I shared a chart showing how generation capacity utilisation has dropped, from 55% in 2000 to 35% today, and is expected to drop further to about 25% by 2035 (the target date for decarbonisation of UK power). While intermittency contributes to most of this reduction, the need for back-up power adds to the “inefficiency”. Globally, renewables are the answer, but the ability for the UK to become energy self-sufficient is questionable, and planning must include both imports and interconnectors.

Renewables will influence daily, even hourly, pricing, and, once we have surplus, they will become the retail marker. Strike prices under Contracts for Difference contracts will be honoured, but pricing must be established for back-up capacity, and at what price will surplus power be sold for electrolysis? Power analytics provider Aurora, in their modelling for the National Infrastructure Commission,3 considers a creaming curve of supplies, but this has yet to be translated into pricing policy and requires transparency of future system operation.

Hydrogen is definitely required for industry and some transport applications and, as shown below, it is also required to support renewables and manage consumer demand. It will provide system flexibility and become a traded commodity, and so longer-term plans can include imports (ref: Japan4 and Germany’s5 planning). Subject to managing of fugitive emissions, initial demand can be met by blue hydrogen as part of the transition from fossil fuels, later to be replaced by green hydrogen as we secure more renewables.

Biomass and Nuclear also figure in the future resource mix; biomass to meet niche demands such as aviation, with nuclear providing baseload capacity. However, costs for nuclear must drop, perhaps through small modular reactors (SMRs), for it to become a mainstream option. Fusion may offer something for the second half of the century.

Energy demand

Industry is already on a path to change through the government’s Industrial Cluster programme, though business models still need more work, especially when compared to the support being offered by the US (IRA) and EU (Green Deal). I also considered the plans for heavy transport in a prior feature. Reducing demand must remain a key priority.

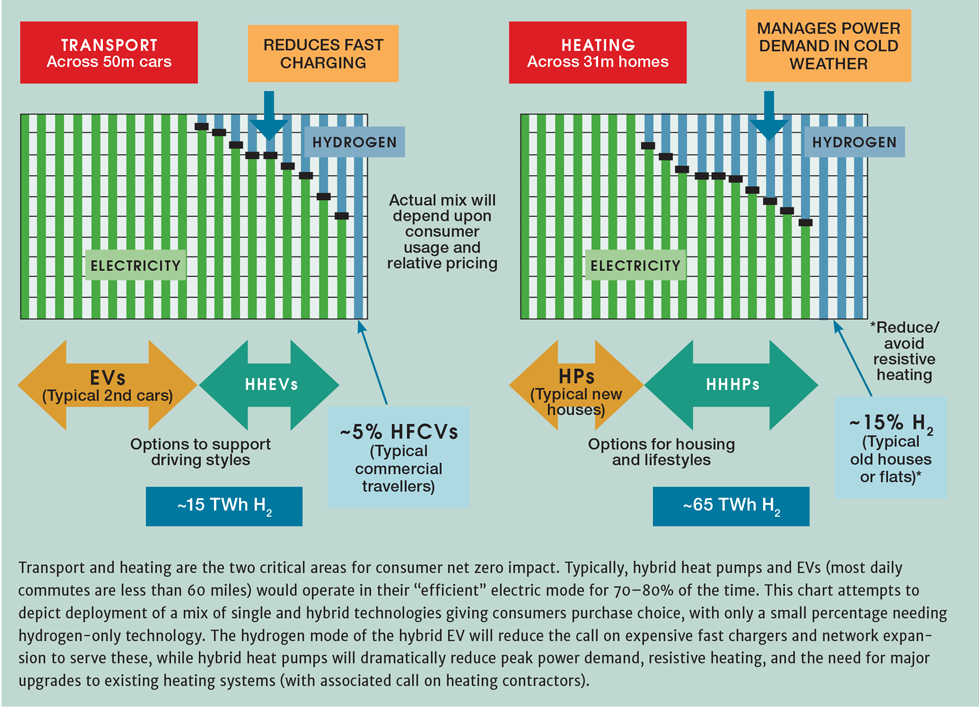

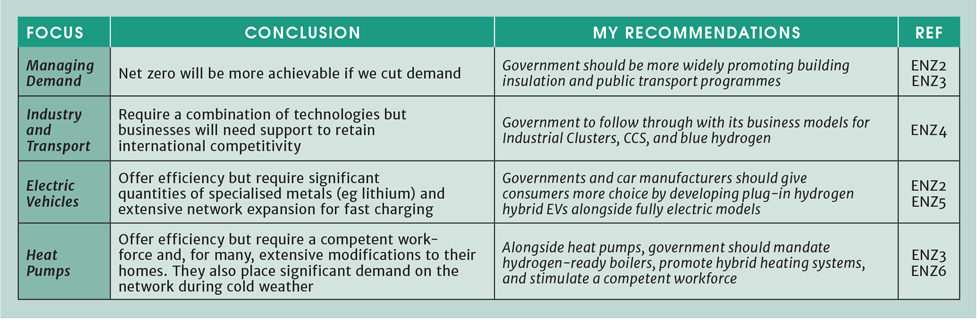

The silver bullets for the consumer transition, EVs and heat pumps, are far from certain. As I discussed in earlier features, these technologies require consumers to make significant changes to their lifestyles and carry “stings in their tails”, stressing power networks at peak times. Consequently, along with measures to reduce demand and the impact of base technologies, I have proposed deployment of hybrid alternatives, combining the efficiency of electricity with the flexibility of hydrogen, giving consumers more choice and reducing the call on resources such as rare metals and lithium. A hydrogen hybrid heat pump has been demonstrated in Wales, while Renault and others have prototype hydrogen hybrid cars. Figure 3 helps explain how hybrid solutions could be included in the future technology mix.

I have estimated the deployment and usage mix to calculate an annual hydrogen demand for the two sectors. This would be in the order of 65 TWh and 15 TWh respectively for heating and transport hybrids and I will demonstrate how this can be supplied in the next section.

Energy networks, balancing, and storage

Networks are designed to receive supplies and meet demand. As we have seen, supplies are intermittent while demand is seasonal, so they must include load balancing and energy storage.

Let me first address storage, discussed in my last feature under energy security. I presented a chart showing the applicability of alternative storage technologies as a function of discharge time and capacity. Short-term energy storage can be achieved utilising batteries, and their technology is continually improving. They can also be supported by smart meters and controls allowing, for example, “smart” EVs to optimally charge automatically and provide vehicle to grid flexibility.

Long-term energy storage to cater for seasonal demand and renewables intermittency requires much more thought. Today the EU holds about 1,000 TWh in dedicated gas reservoirs to manage winter gas and power demand (compared to the UK’s 10 TWh), and in a recent report6 the Royal Society (RS) estimates that by 2050 between 50–100 TWh energy storage must be deployed alongside intermittent renewables to meet demand.

However, it too has a sting. It is implausible for this to be stored in batteries, and so they considered a range of storage vectors, concluding that hydrogen stored in new or existing solution-mined salt caverns is most economical. There is an efficiency loss through the hydrogen cycle of electrolysis, storage, and utilisation, but other modelling studies (eg Aurora) similarly consider hydrogen for back-up energy, and despite the 50–80% cost premium for this back-up (ref: Figure 14 in their report), the RS still evaluate renewables to be lower cost than either nuclear or e-fuels.

Centrica are studying options to convert their Rough gas storage facility to hydrogen service, providing up to 17 TWh of geological storage, and, due to scale, I believe this will be cheaper than caverns. Whichever way we go, energy storage will require significant financial engineering to fund.

Moving to system balancing (depicted on the left-hand side of the energy schematic); in March the government announced measures to address this by considering renewal of some of our gas-fired power generation to maintain energy security during periods of low renewables output. This is an encouraging first step but as the environmental lobby point out this is not the complete answer, for this still relies on fossil gas. Ultimately, system balancing will be accomplished through the “hydrogen cycle” harnessing surplus renewable energy on “good” days to produce hydrogen and using this to provide back-up power when demand is high and/or renewables are underproducing. Today this is not of major concern, for balancing is achieved by turning on or off natural gas CCGT or older nuclear plants, and any replacement power plants must be designed for hydrogen service.

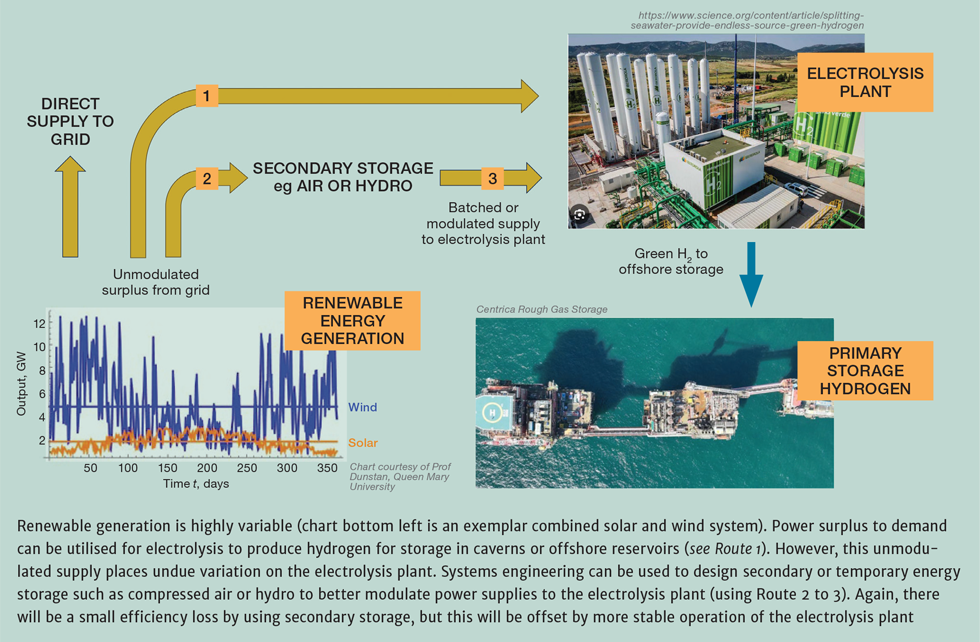

We are already network constrained on some windy days, and, as the percentage of renewables gets closer to 100%, surpluses will increase but they can be used to produce green hydrogen at low cost. This is where system engineering can really come to the fore, as we must find economical solutions. The hydrogen cycle is inefficient, but it will be driven by differential electricity pricing (ie low prices at times of excess generation to higher prices at times of shortfall). And, while there will be an overarching summer to winter spread, wind energy varies hour by hour, and these shorter variations will impact the operation of electrolysis facilities, further reducing viability. See Figure 4 for an example of how systems engineering can help increase the efficiency of electrolysis operations.

At this stage, only limited thought has been given to electrolysis, and systems optimisation is essential. Initially, costs will be high, but as we experience larger surpluses, costs will drop. Indeed “surplus” hydrogen, as I term it, will be valued at the prevailing market price, and so owners of electrolysis plants will likely demand a regulated rate of return for their service.

The other side of the coin is when hydrogen is drawn from store to cover shortfalls in generating capacity (during periods of low renewables and/or very cold weather). The simple answer would be to convert combined cycle gas turbine (CCGT) plants to operate with hydrogen.

However, CCGTs (50+%η) are not adept for peak-shaving, as combined cycle units require longer ramp-up times and stable operation, and many plants are reaching the end of their design life. Some capacity can be provided this way, but replacement plants will likely be reciprocating (recip) engine plants (+/-40%η) as these offer more functionality. Most system modelling studies estimate that we will require anywhere between 20–40 GW of recip capacity, but as yet they are not available and again the business model needs to be established. The lower operating efficiency of recips further reduces the efficiency of the hydrogen cycle.

When writing my features on hybrid technologies I had not considered the fact that we require up to 100 TWh hydrogen to cover renewables intermittency. Instead of burning hydrogen in new recips at low efficiency, we can reduce peak power demand by operating hybrid heat pumps and EVs in their hydrogen mode. These use hydrogen more efficiently and the 80 TWh I calculated can be matched to a greater or lesser degree by that held in store to manage renewables intermittency – the penny dropped.

So, this brings us back to networks. We will require a significant upgrade and expansion of our power network to cater for the growing demand and intermittency, while we will still need a basic hydrogen network to guarantee supplies to Industrial Clusters. Modelling studies have compared converting all homes to electrified heating with converting the existing natural gas network to supply hydrogen. Most conclude that full electrification is optimal and simpler to implement, though Imperial College London studies7 indicate that gas grid conversion and hydrogen heating would be cheaper. As mentioned, none of the recent studies include hybrid technologies, and I believe these offer the lowest cost, higher efficiency, more redundancy, and the highest chance of consumer acceptance.

Considering my future energy schematic, we can balance supplies outside the demand envelope using recips for peak power, or inside using hybrid technologies. The first option will require a tripling of the power grid, while the second option requires a doubling of the power grid and full conversion of the gas grid.

Proponents point to the total electrification implemented in Scandinavia and Canada, but these regions already had significant hydropower storage schemes. Others recommend oversizing renewables capacity to avoid investment in the hydrogen cycle, curtailing it at times (we already do this occasionally due to network constraints). Indeed, think tank RethinkX believe this will be economically viable across much of the US. But as I have indicated, in the UK the cost-effectiveness of renewables has already started to bottom, and the economics of “wasted” energy will not prevail.

Here in the UK, we have an excellent gas network, which over recent years has been upgraded to extend its life. As I have discussed previously, conversion will take time, come with a cost, and require appropriate safety engineering. However, we must remember that Coal Gas, used up until the 1960s, contained a significant proportion of hydrogen.

Implementation

I believe the future energy schematic that I have proposed will help us systems engineer net zero. I also hope it provides a clearer picture of how we can get electricity, hydrogen, and e-fuels working together to realise lower costs for consumers and cancel out the “stings in the tails” of renewables, heat pumps, and EVs by balancing demand both inside and outside the demand envelope.

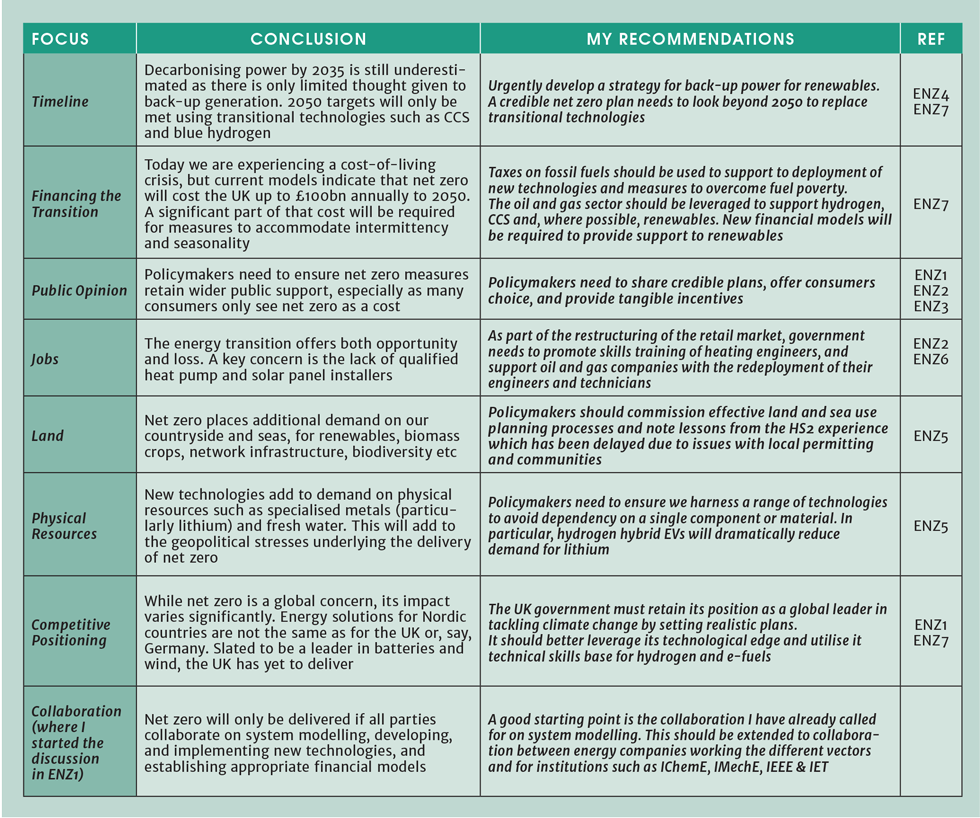

My Engineering Net Zero journey has addressed the overall timeline, financing the transition, managing public opinion, impact on jobs, considerations for land use and physical resources, international competitive positioning, and, finally, the need for that collaboration, and further conclusions and recommendations are summarised below.

In a recent meeting, Goran Strbac, professor of energy systems at Imperial College London, confirmed that engineers and policymakers still have widely differing views on what is needed to deliver net zero. So, I hope this analysis can help us break down preconceived opinions on electricity versus hydrogen, to deliver the benefits of both to wider society. Hybrid solutions demand more system analysis, and so it is essential that chemical engineers use their skills to deliver a credible and more consumer-friendly alternative for net zero.

We need a “Resources to Market Plan” which gives consumers choice and avoids the risk of a monoculture solution. Today's energy is multi-vectoral and global, it will still be that tomorrow.

References

1. www.thechemicalengineer.com/tags/engineering-net-zero-series/

2. https://bit.ly/3VntWcK

3. https://bit.ly/43jOuoC

4. https://bit.ly/3wTzEsI

5. https://bit.ly/4aaZw1p)

6. royalsociety.org/electricity-storage

7. https://bit.ly/3x37mMc

Recent Editions

Catch up on the latest news, views and jobs from The Chemical Engineer. Below are the four latest issues. View a wider selection of the archive from within the Magazine section of this site.