Five Questions for Kwasi Kwarteng about the UK's Hydrogen Strategy

The UK Government published its Hydrogen Strategy in August with an accompanying media fanfare. It commits the UK to a twin track approach of using blue and green hydrogen – blue being methane reforming with CCS, and green using renewable power to electrolyse water.

Page 14 of the strategy says a key principle is: “Long-term value for money for taxpayers and consumers: To deliver value for UK taxpayers and consumers we will seek to minimise the cost of action, and drive down costs over the long term, as we reach for our 5 GW ambition and beyond to CB6 (6th Carbon Budget) and net zero.”

As a taxpayer and consumer, I am very keen to know how hydrogen will impact on my fuel bills and how that would compare with an electrification pathway. After reading the strategy, there are five questions I’d like to put to Kwasi Kwarteng, the Secretary of State at the Department of Business, Energy and Industrial Strategy (BEIS):

Question 1

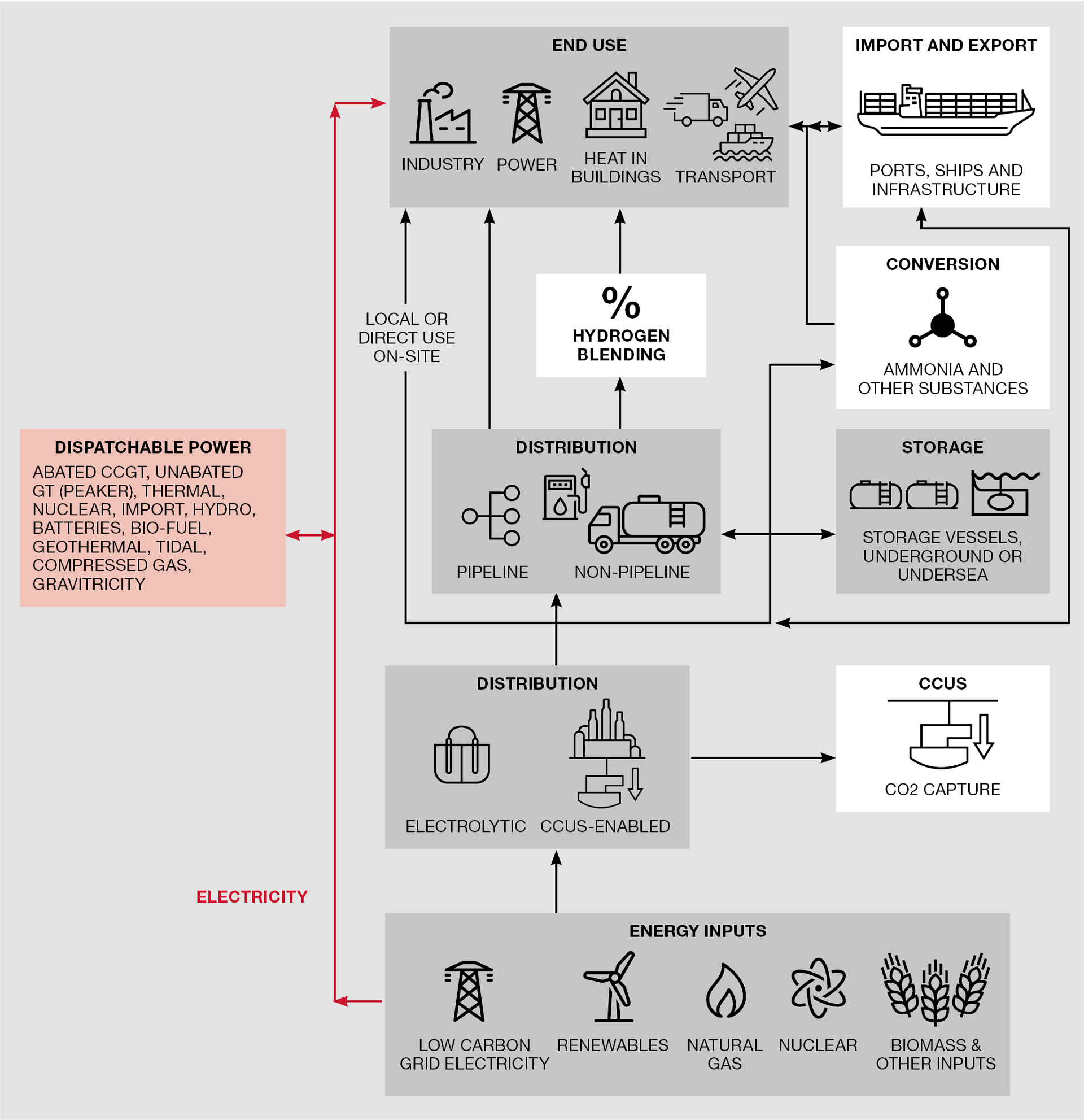

Here is the hydrogen value chain from page 22 of the strategy. I’ve placed the electricity pathway alongside it in red.

The electrification pathway has much fewer energy vector changes and will therefore be much more efficient. That will require significantly less low-carbon electricity. Of course, it will also require grid upgrades, but I would expect an electrification pathway to show significant benefits for the taxpayer in terms of cost, together with a much smaller environmental footprint.

The first question I would like to ask Mr Kwarteng is: “Can you provide a quantified, holistic, risk- and sustainability-based comparison of the two pathways to convince me that hydrogen is a better solution for consumers and taxpayers than electrification, including electricity driven heat networks?”

Without the comparison, it’s hard for this engineer to believe that hydrogen is the right choice for delivering long-term value for money to UK taxpayers and consumers.

Question 2

Transport is a very large source of greenhouse gas emissions, with the passenger car being the major contributor. Decarbonising this mode of transport is clearly key to achieving net zero. I could find little reference to the hydrogen fuel cell electric vehicle (HFCEV) in the strategy. I have previously shared my views with a comparison of a HFCEV and a battery electric passenger car (BEV). To my mind the BEV is a far superior option.

If the UK Government is of a similar view, what does that mean for proponents of HFCEV like Toyota and Element 2? Should they be questioning their investment?

Therefore, the second question I would like to ask is: “Does the lack of reference to hydrogen-fuelled vehicles mean the UK Government judges hydrogen as a poor choice in comparison to the battery electric vehicle?”

Question 3

The production of hydrogen provides a chemical precursor for ammonia, fertilisers, methanol, and as a conditioning agent for liquid fuels. It is also used in the metals and glass industry. Grey hydrogen production in the UK dominates. This is where steam is used to reform natural gas, but the resulting CO2 is not captured and is instead emitted to the atmosphere. The UK currently produces around 700,000 t/y of hydrogen using this unsustainable method. As no CO2 is captured, grey hydrogen emits around 9 t of CO2 per tonne of hydrogen produced. That is 6–7m t/y of CO2 plus the associated emissions of methane from the extraction, conditioning, transportation and hydrogen conversion process.

Blue hydrogen will capture around 90–95% of CO2 emissions, which I welcome. The UK imports much of its natural gas and as a result of the inefficiencies associated with blue hydrogen production, means that gas imports will have to be increased.

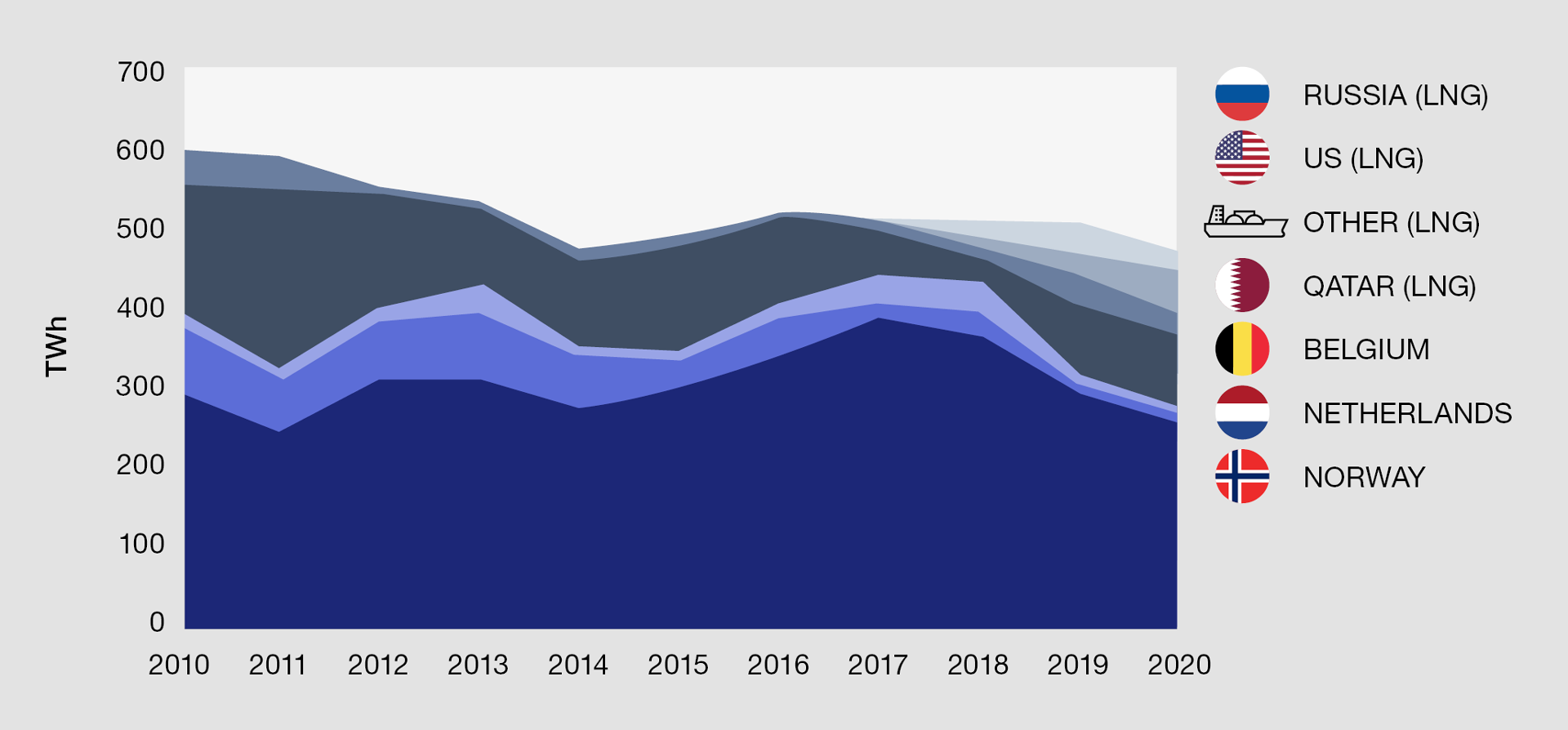

Last year’s gas import figures are shown below. In my experience, the associated CO2 and methane from Norwegian gas will have been well managed. But what about the non-Norwegian gas?

The importance of emissions control is paramount when using blue hydrogen. On a 20-year lifetime, methane has a global warming potential of around 80 times that of CO2. If GHG emissions are poorly managed the benefits of blue hydrogen and its carbon capture will be eroded. Therefore, my third question for Mr Kwarteng is: “Have the supply chain emissions for imported methane/LNG been accounted for when quantifying the benefits of blue hydrogen?”

Question 4

The strategy makes numerous mentions of using a 20% v/v hydrogen blend in the existing gas network. An energy balance shows that that for every tonne of blue hydrogen blended there will be around 6 t of CO2 saved. No bad thing. But, as previously stated, grey hydrogen produces around 9 t of CO2 per tonne of hydrogen.

The fourth question for Mr Kwarteng is: “Would it not be better for the UK to prioritise replacing current grey hydrogen production before using blue hydrogen for blending?”

That would provide a larger UK GHG saving than using blue hydrogen for fuel.

Question 5

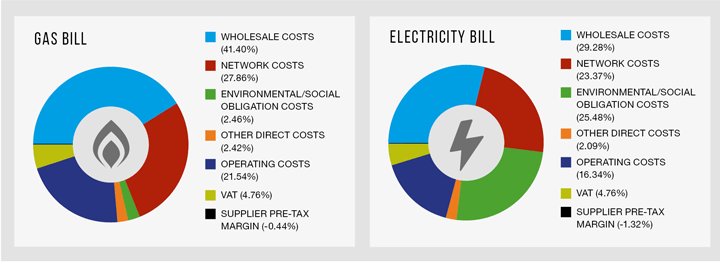

It is clear from the strategy that significant amounts of taxpayers' money will be directed at hydrogen. Ofgem’s breakdown of gas and electricity bills are shown below. As can be seen, electricity carries a much higher environmental/social obligation cost: 25% as opposed to 2% for gas.

Ofgem states: “these costs could cover schemes to support energy efficiency improvements in homes and businesses, help vulnerable people and encourage take-up of renewable technology.”

My own research suggests that blue hydrogen will be around twice the retail cost of natural gas for domestic consumers – a very worrying outcome as it will push many more families into fuel poverty. Furthermore, if the wholesale cost of fuel rises, the obvious consequence will be an increase in the cost of manufactured goods.

My final question Mr Kwarteng is this: “Will the social/environmental cost for gas be increased to pay for the development of hydrogen in the way it was used on electricity bills to pay for wind development and other renewable electricity initiatives? If so, what will happen to my gas tariff if I use blue or green hydrogen?”

On a more general note, the strategy was hailed by some stakeholders as providing much-needed certainty. That position is lost on me, as I counted in the strategy 44 “mays” and 114 “coulds” with respect to hydrogen. Much is also made of providing 5 GW of blue and green hydrogen by 2030. That is only 2–3% of today’s energy mix. Hence, the contribution of hydrogen to net zero UK will be very minor in the next decade. Yet most climate scientists are saying that action is needed now.

IChemE has also called for immediate action in its position on Climate Change. Here it is stated: “We agree that serious action to combat climate change is urgent and must start immediately and accelerate. IChemE will work with associated industries and governments to achieve the rate of change needed to remain below 1.5°C. The IPCC articulates this as reducing global anthropogenic greenhouse gas (GHG) emissions by at least 7.6% year on year to 2030 (as an interim target) or reducing total emissions by at least 50% each decade from now to 2050.”

I’m left thinking that the UK’s Hydrogen Strategy is an evidence-weak distraction to much-needed immediate material action. What might that be? Ask me the question of how to drive down emissions in the most efficient manner and in the interests of taxpayers and my answer is: “Electrify transport and heat; increase the energy efficiency of our homes, businesses and industries; implement a smart energy grid; and boost the use of renewables and biofuels.”

Recent Editions

Catch up on the latest news, views and jobs from The Chemical Engineer. Below are the four latest issues. View a wider selection of the archive from within the Magazine section of this site.